January 1 marks the beginning of a new year, but for many, it also symbolizes changes we commit to making in our lives. A new year is the perfect time to implement a positive change, and it’s the perfect time to evaluate your finances.

Obtaining the peace of mind financial stability brings begins with knowing exactly where you stand. Your financial resources affect not only your ability to achieve your goals, but also your ability to protect these goals from potential crises. The steps are simple – just maintain the resolve.

Step 1: Determine the value of you.

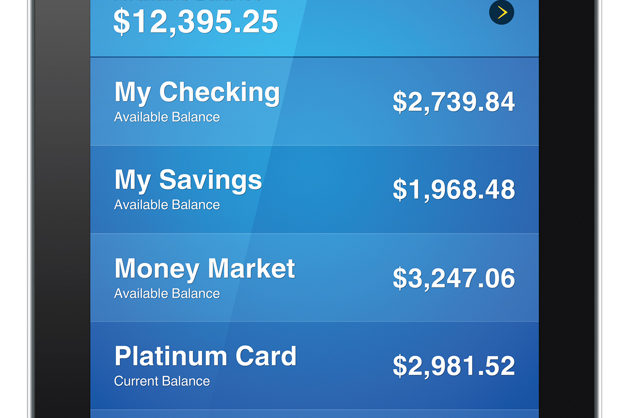

You can’t implement any financial plan until you know your net worth. Your net worth is simply the total of your assets (what you own) minus your liabilities (what you owe). Assets include personal possessions, vehicles, homes, checking and savings accounts and the cash value of any life insurance policies you may have. Include the current value of your investments, such as stocks, real estate, certificates of deposit, retirement accounts and IRAs, and the current value of any pensions.

Liabilities include the remaining mortgage on your home, credit card or student loan debt, taxes due on investments or any other outstanding bills. Subtract your liabilities from your assets. The goal is to create positive net worth, which is part of what you will draw on to achieve your financial goals.

Step 2: Reassess your situation.

Your monthly family budget begins with your net pay, from which you then deduct all your fixed monthly costs like mortgage/rent, utilities, car and car insurance payments and estimated costs such as gasoline, groceries and clothing. From here you can build or reassess your budget. Net income often changes from year to year even if your gross wages remain the same. Benefits and other payroll deductions may fluctuate, so it’s important to review your budget accordingly.

Step 3: Lose the debt weight.

The most significant way to improve your financial health is to create a plan for paying off any debt sources… and stick to it. Include debt payments in your monthly budget. Paying off the least expensive bills first will quickly reduce the number of entities to which money is owed and give the feeling of progress, making it easier to stay on track.

Step 4: Make a stash.

Once debt has been paid off, families should save the equivalent of at least three months’ salary to plan for emergencies (health care-related costs, loss of a job, etc.). Keep the money in an interest-bearing savings account.

Step 5: Plan ahead.

If you need to build credit or re-establish credit, many financial institutions offer credit-builder loans that will help you establish good borrowing histories. Consider meeting with a financial advisor to create a roadmap of your financial future that leads you to your goal. Bonus: your advisor can help you implement a system to make tax filing easier as well.

Every Step of the Way: Go digital.

If you haven’t already, make sure you are signed up for mobile and online banking. Set up auto-pay to avoid late fees on bills, and download smartphone apps to keep real-time track of your finances.

Suzanne Symcox is executive vice president of First Fidelity Bank, N.A., a locally owned full-service community bank established in 1920.